MYR 1 →

MYR 1 → USD: 0.2358

USD: 0.2358  SGD: 0.3036

SGD: 0.3036  EUR: 0.2083

EUR: 0.2083  THB: 7.6927

THB: 7.6927  KRW: 323.1171

KRW: 323.1171  CNY: 1.6972

CNY: 1.6972  JPY: 33.6755

JPY: 33.6755

Hey there, fellow Malaysian investors! Thinking about jumping into PMCK Berhad’s IPO? Let’s break it down so you can decide if this healthcare player fits your portfolio.

What’s the Deal? PMCK (Putra Medical Centre Kedah) is going public :

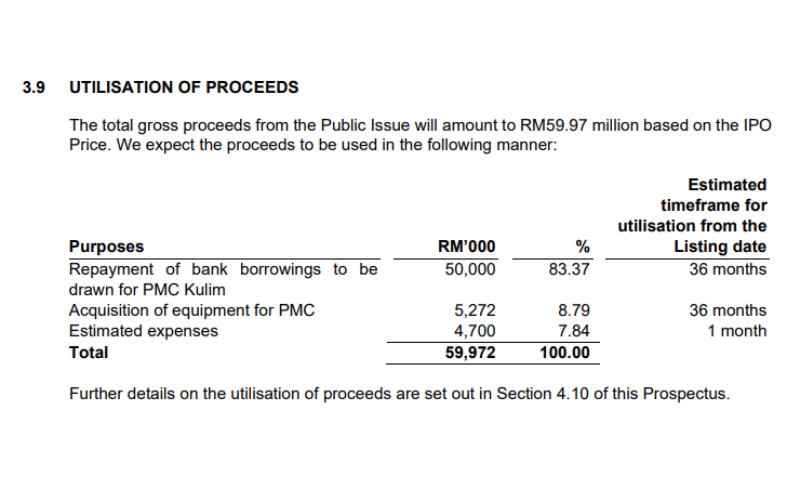

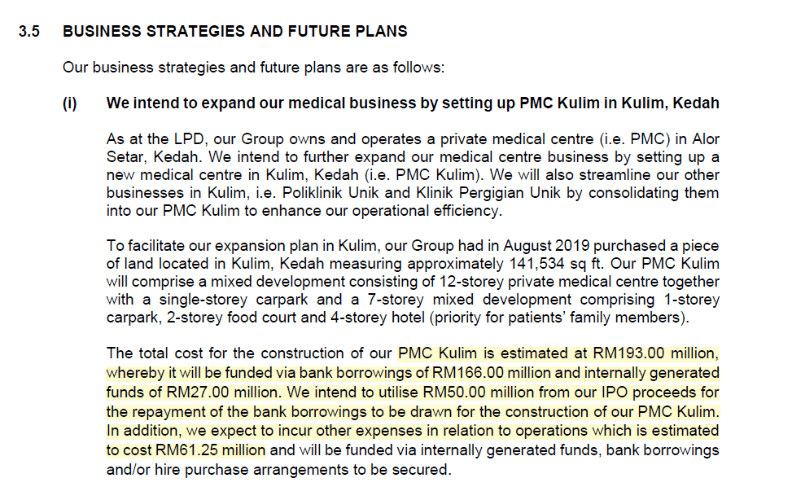

offering 272.6 million new shares at RM 0.22 each. The IPO will raise RM 59.97 million, mainly to pay off loans and fund a new hospital in Kulim. They’re also buying medical gear and covering listing costs.

Where’s the Money Going?

- RM 50 million (83%) to repay loan for new PMC Kulim (a 180-bed hospital under construction)

- RM 5.27 million (9%) for equipment in Alor Setar’s hospital

- RM 4.7 million (8%) for listing expenses

Strategic Moves Besides the cash flow, PMCK wants to raise its profile, bring in more investors for future fundraising, and let staff and the public own a piece of the action. Smart, right?

What Does PMCK Actually Do?

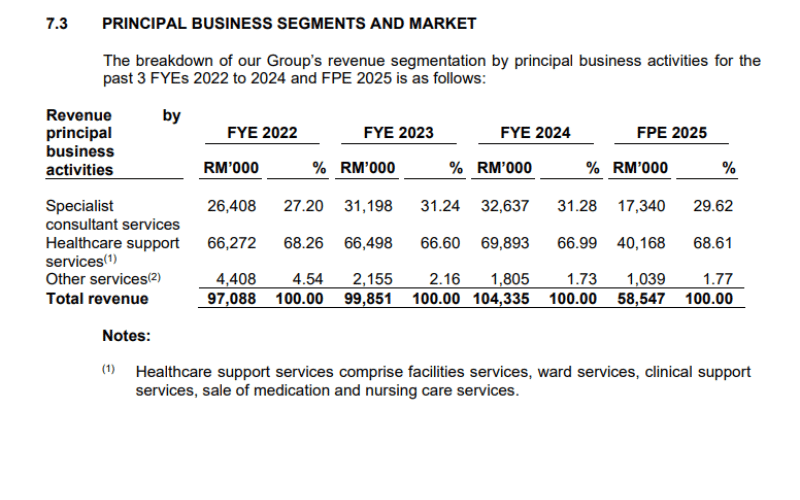

They run a 162-bed hospital in Alor Setar and offer:

- Specialist treatments (surgery, medicine)

- Support services (wards, pharmacy, diagnostics)

- Extra services like dental, polyclinic and new lab biz (RYM DX)

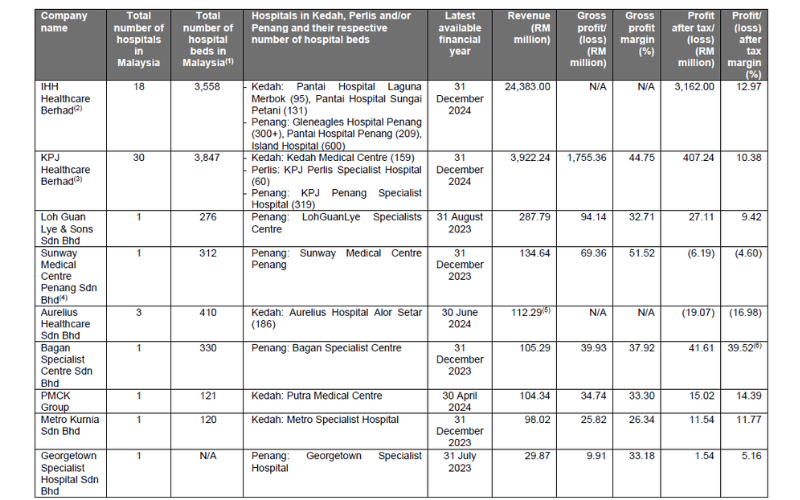

They’re also on panels for 7 insurers, 12 TPAs, and 49 corporate/government programs—meaning a reliable stream of patients. FY2024 saw a 71% bed occupancy rate. That’s solid!

Strengths You’ll Love

- Big presence: 24% of Kedah’s private beds

- Trusted payor network = steady patients

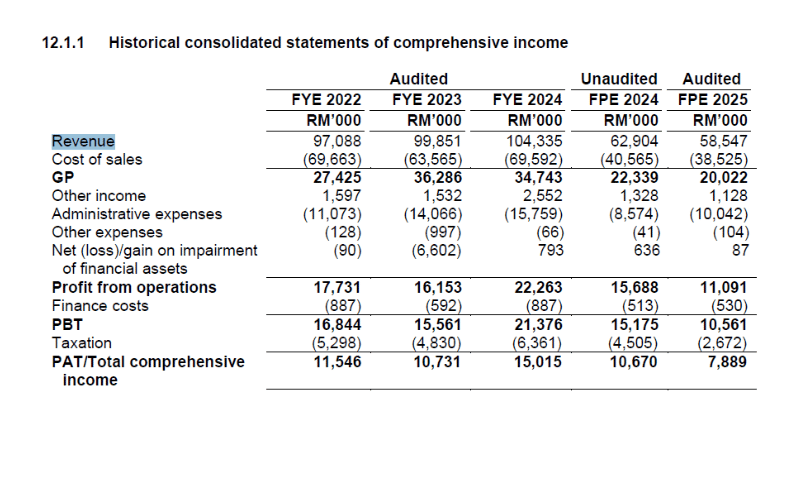

- Profitable: RM 104.3 mil revenue, RM 15 mil profit (14.4% margin)

- Founders still hold 70% after IPO (they’re in for the long game)

- Hard to replicate: licensing, capital, etc.

But There Are Some Weak Spots

- 99% of revenue comes from Alor Setar

- Risky if licenses get delayed or there’s a flood (like in 4Q 2024)

- Hard to hire good doctors and nurses

- High gearing (0.92x) until IPO funds come in

Growth Opportunities Ahead

- PMC Kulim will double the bed count (target 2027)

- Riding the wave of ageing population + medical tourism from Penang/Langkawi

- Diagnostics lab biz = better margins

Red Flags to Watch

- Gov’t may introduce fixed-price hospital fees (DRG system)

- Big boys (IHH, KPJ, Sunway) entering northern Malaysia

- If Kulim build is delayed, finances will be stretched

- Any new policy that limits insurance claims could hit income

The Numbers That Matter

- FY2024 revenue: RM 104.3 million

- Profit after tax: RM 15 million

- Net gearing before IPO: 0.17x

- Current ratio: 3.8x

- Bed use: 71% from 162 beds (42,132 patient-days)

IPO Snapshot

- Shares: 272.6 mil new + 32.7 mil offer-for-sale

- Price: RM 0.22

- Market cap: ~RM 240 million

- PE ratio: 15.9x based on FY2024 earnings

- Listing: 9 July 2025 (apps close 25 June)

TL;DR? PMCK is your chance to own a slice of a profitable, Kedah-based hospital with plans to expand to Kulim. It’s a niche player with strong insurer ties and healthy margins. But the risks are real: licensing, manpower, and heavy reliance on one location.

Investor Tips! ✅ Great for investors seeking healthcare exposure in Malaysia’s north ⚠️ Monitor Kulim project closely—it’s the big growth driver ❗ Keep tabs on health regulations and insurance payment trends

So, geng, what do you think? Would you back a regional hospital group aiming to grow its footprint and double its capacity in a booming area? Let’s discuss in the comments! 💬

For more blog : visit Stooper’s business talk